Peak TV may have already peaked, as the recent Hollywood strikes have impacted the delivery of fresh scripted content over recent months. Which is why no one is arguing that the entertainment industry is still in the unfettered Wild West phase that drove its prolific expansion from 2018-2022.

As such, studios are aiming for a much more efficient allocation of programming resources with the goal of generating more consistent returns on content investments. In other words, building a library of movies and TV shows that all contribute to overall platform success is integral. No more mooching!

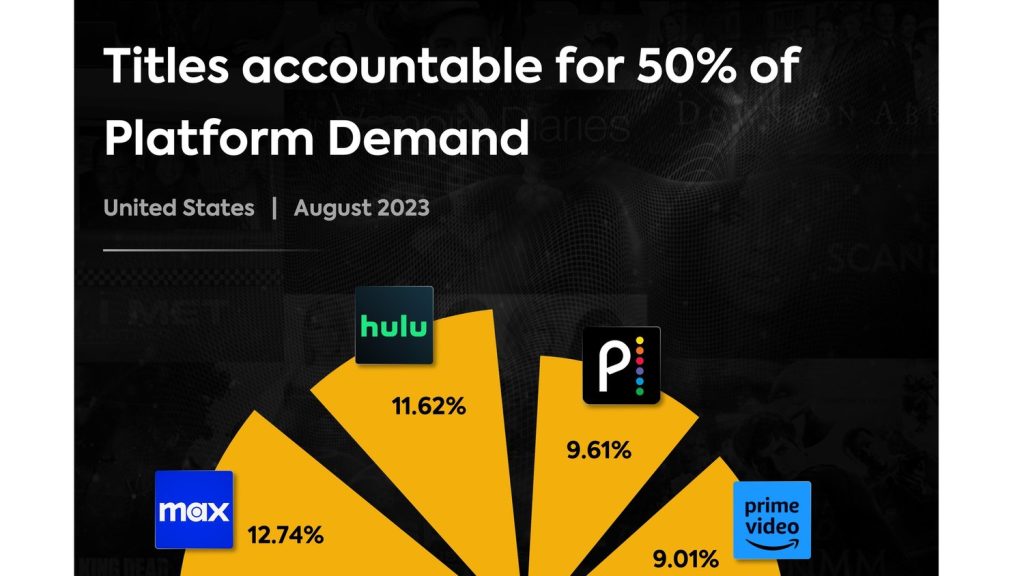

The chart below displays the percentage of shows and movies (both licensed and original) accounting for 50% of the total demand for each major streaming service in the US in August, according to Parrot Analytics.

This metric gauges how audience demand is spread across various titles by platform. A higher percentage of titles accounting for 50% of total demand reflects a more even distribution, meaning that a larger number of shows and movies are resonating with audiences and generating a positive return on investment. A lower percentage reflects a more top heavy library in which demand is largely driven by a smaller crop of titles or, in less scientific terms, these streamers are putting a lot of eggs in one basket.

Again, summer release schedules were partially disrupted by recent labor stoppages. Yet Netflix still released 45 new TV titles (both licensed and original) in the US in August, according to What’s on Netflix. Despite the market-leading streamer’s prodigious domestic library, just 8.02% of its US catalog accounted for 50% of its total demand that month. This is a more concentrated and tightly packed demand distribution than one might expect from the prolific Netflix.

Conversely, Disney+ has a much smaller library than Netflix, yet the second-largest percentage of total titles that account for 50% of its US demand that month (14.66%). Though the streamer is looking to generate more hits outside of the Marvel and Star Wars franchises, it’s clear that the volume of shows produced across Disney+’s major IPs boast an extremely high floor. This helps in generating strong guaranteed demand across the two core franchise brands and key kids programming lanes.

Ultimately, this chart helps to underline where strategic library expansion and double down opportunities may lie by platform.