To print this article, all you need is to be registered or login on Mondaq.com.

Rapid Changes, Rapid Upheaval

The Media & Entertainment (M&E) industry is undergoing

rapid changes in many different dimensions which are impacting all

aspects of the video ecosystem, upending business models and

affecting consumer consumption and technology delivery models.

From an economic perspective, the “free money era” is

over. Lower interest rates helped to fuel Cable TV expansion with

continued MVPD carriage fee increases, escalating sports rights

fees, expanded film slates and funded the build-out of streaming

platforms. Today, however, all of those drivers that fueled M&E

growth are challenged. MVPD carriage fees for linear TV are in

decline. The lucrative business of home video, comprised of rentals

and purchases which subsidized the film industry, continues to

dwindle. Higher interest rates challenge M&E firms in servicing

the existing debt on their balance sheets and impact the ability to

support growth driven by debt-fueled M&A. Macro-economic issues

such as inflation and higher interest rates along with labor

strikes, cord-cutting and intense competition among streaming video

providers have resulted in significant structural changes to the

entire M&E ecosystem.

The industry economics are eroding, consumers are changing their

behavior and technology is advancing at a pace at which the

industry has never experienced. In view of all of these factors,

mergers and acquisitions to drive industry consolidation through

cost optimization, the adoption of new target operating models and

the execution of carve outs to divest non-core assets will define

the M&E business operating agenda for the next 12-24

months.

What Corporation Transformation Initiatives Are Impacting the

M&E Industry?

Almost every week, there are significant developments in the

M&E industry involving corporate transformation. Large

technology companies are purchasing broadcast rights to sporting

events that heretofore were only available on major broadcast

networks or Pay-TV channels. Streaming service providers are

removing programming for lower performing shows and sophisticated

algorithms are being used to provide information about how program

budgets are sized, authorized and executed across the global

marketplace.

Relative to what they were five years ago, many balance sheets

are now significantly more burdened. Acquiring long-term content

rights, increasing original scripted production and a blank-check

mentality for building out global streaming platforms appeared to

be a logical strategy to drive growth. But viewers shifted, Pay-TV

subscriptions decreased and viewers went shopping for selective

streaming subscriptions. However, consumer churn rates on streaming

services are significantly higher than historical MVPD churn rates,

thus making commitments to long-term sports rights and increased

original programing investments challenging to sustain.

The Macro Time Horizons in M&E

Ask anyone who has had a senior level position across any

M&E segment—film, television, music, etc.—what the

pace of change was over the course of 50 years (1960 to 2010) and

the response would probably be the notion that while there were

very significant changes during that period, they were also gradual

and accretive. Today’s changes are anything but that.

- In television, three broadcast channels per market grew to

hundreds via Pay-TV services. Network television was joined by

cable networks and the expansion of channels via the cable bundle,

home video (VHS/DVD), electronic sell through (EST) and video on

demand (VOD) all added new content windowing to drive incremental

revenue. - In Film, the box office expanded as theaters evolved into

multiplexes which led to the globalization of content with new

markets and territories as well as creating additional windows for

monetization such as Pay-TV, home video, VOD, EST and Premium VOD

for same day and date releases. - Streaming platforms were assumed to be a further extension of

monetizing the video ecosystem on a global basis, through

direct-to-consumer, subscription and ad-supported services.

However, the technology and the business models supporting

streaming have proven to be more transitory than accretive.

Streaming shifts audiences from traditional “cash cow”

businesses such as linear television but it is a lower margin,

higher churn and highly competitive offering. Streaming does not

currently provide the accretive revenue and margin pathways that

prior evolutions in the video ecosystem provided.

The evolution of those accretive windows and technologies for

incremental distribution played out over decades. But change is

accelerating and M&E is now competing with hyperscaler

technology platforms, their significant balance sheets and cash

reserves, as well as traditional M&E competitors.

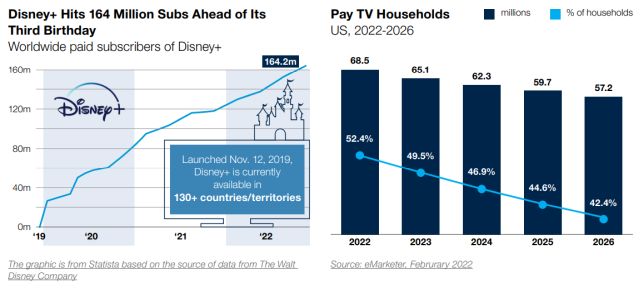

It took Netflix 10 years to reach 100 million subscribers. It

took Disney+ 16 months to reach 100 million subscribers. After

decades of growth, cable service providers will continue to

experience losses in Pay-TV subscribers. According to audience

measurement firm Nielsen, U.S. TV-viewing time as of November 2023

was led by Streaming at 36.1 percent followed by Cable at 28.3

percent and Broadcast at 24.9 percent.

Driven by Wall Street’s mandate to measure media success via

digital platforms and a growth at all cost mentality, there has

been an incessant march to create streaming video services and to

establish direct-to-consumer relationships. Consumers struggle with

having to subscribe to multiple streaming services to watch desired

content. The challenge of content discovery is considerable. The

onus is now on the consumer to find content as opposed to the

traditional television viewing experience where content is

programmed and delivered for a passive viewing experience. Over

time, recommendation algorithms driven by artificial intelligence

(AI) and machine learning (ML) will assist in solving some of these

problems. Content providers at first enjoyed the revenue gained by

licensing content to streaming providers but then decided to

discontinue those licensing deals as they sought to keep their

content exclusively on their own streaming platforms to drive

subscriber growth. Original content creation and acquisition

budgets measured in the billions of dollars, increasing in double

digit percentages Year-over-Year (YoY).

The objective was clear: Gain as many subscribers as fast as

possible. The result? Hundreds of millions of subscribers

worldwide. But the “grow subscribers at any cost”

approach resulted in billions of dollars spent on creating original

content and building streaming platforms to support global

direct-to-consumer services at scale. The lost revenue from no

longer licensing their content to third parties has also

contributed to billions of dollars of losses in operating these

streaming services. The strategy for content exclusivity on owned

and operated streaming platforms eroded a proven and necessary

content monetization window.

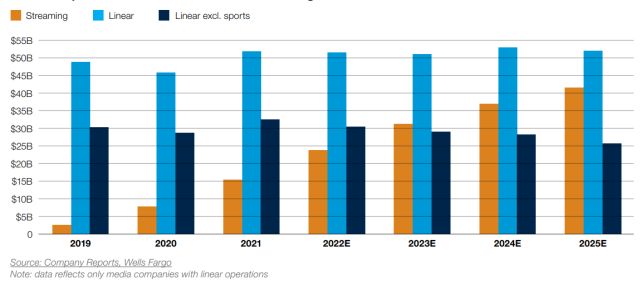

Content Spend Forecast: Linear TV vs. Streaming

And then, a sensibility switch was turned on by Wall Street and

suddenly the new dictum is now profitability over subscriber

growth. The industry has come almost full circle in that it:

- Initially licensed content to streaming services to drive

incremental distribution revenue. - Recognized that content shouldn’t be on a competing service

to assist in driving a competitor’s growth and should be used

to drive subscriber growth on their owned and operated streaming

service platform. - Re-established third party licensing and the associated revenue

as they are important aspects of content monetization and

profitability. - Evolved their content windowing strategy to address when

content should be made available on their own streaming services as

well as licensed to other platforms to maximize distribution

revenue and audience reach.

According to The Hollywood Reporter, original content spend by

streaming providers grew 45% from 2021-2022 but only grew by 14% in

2023 as a result of the renewed focus on the profitability of

streaming services.

To be sure, there are companies in the M&E industry that

have healthy balance sheets and robust cash flow. There are also

numerous companies that are severely leveraged and have flat or

decreasing revenue along with high fixed overhead costs. This

creates significant challenges to generate free cash flow (FCF) to

service the debt, especially in relation to increased interest

rates. And, in many cases, EBITDA of these organizations is still

predominantly driven by their linear networks’ businesses. They

may have technical operations that may be better suited for a cloud

or streaming provider and are facing challenges from a crop of

competitors leveraging the newest technologies and scale to

reinvent current operations at far more advantageous operational

run rates.

To view the full article, click here.

The content of this article is intended to provide a general

guide to the subject matter. Specialist advice should be sought

about your specific circumstances.

POPULAR ARTICLES ON: Media, Telecoms, IT, Entertainment from United States