This article is part of a series from the Center for American Progress exposing how the sweeping Project 2025 policy agenda would harm all Americans. This new authoritarian playbook, published by The Heritage Foundation, would destroy the 250-year-old system of checks and balances upon which U.S. democracy has relied and give far-right politicians, judges, and corporations more control over Americans’ lives.

Nearly three decades of deregulation opened the door for banks, investment companies, insurers, and other firms to engage in the excessive risk-taking that culminated in the 2007–2008 financial crisis. While these financial actors profited handsomely, the costs of their behavior were borne by others. During the Great Recession that followed, the United States experienced the most significant sustained job losses since the Great Depression, which worsened wealth gaps between the middle class and wealthy Americans. To address this, Congress passed the Dodd-Frank Act in 2010, to curb the excesses of the financial institutions that brought the economy to near collapse.

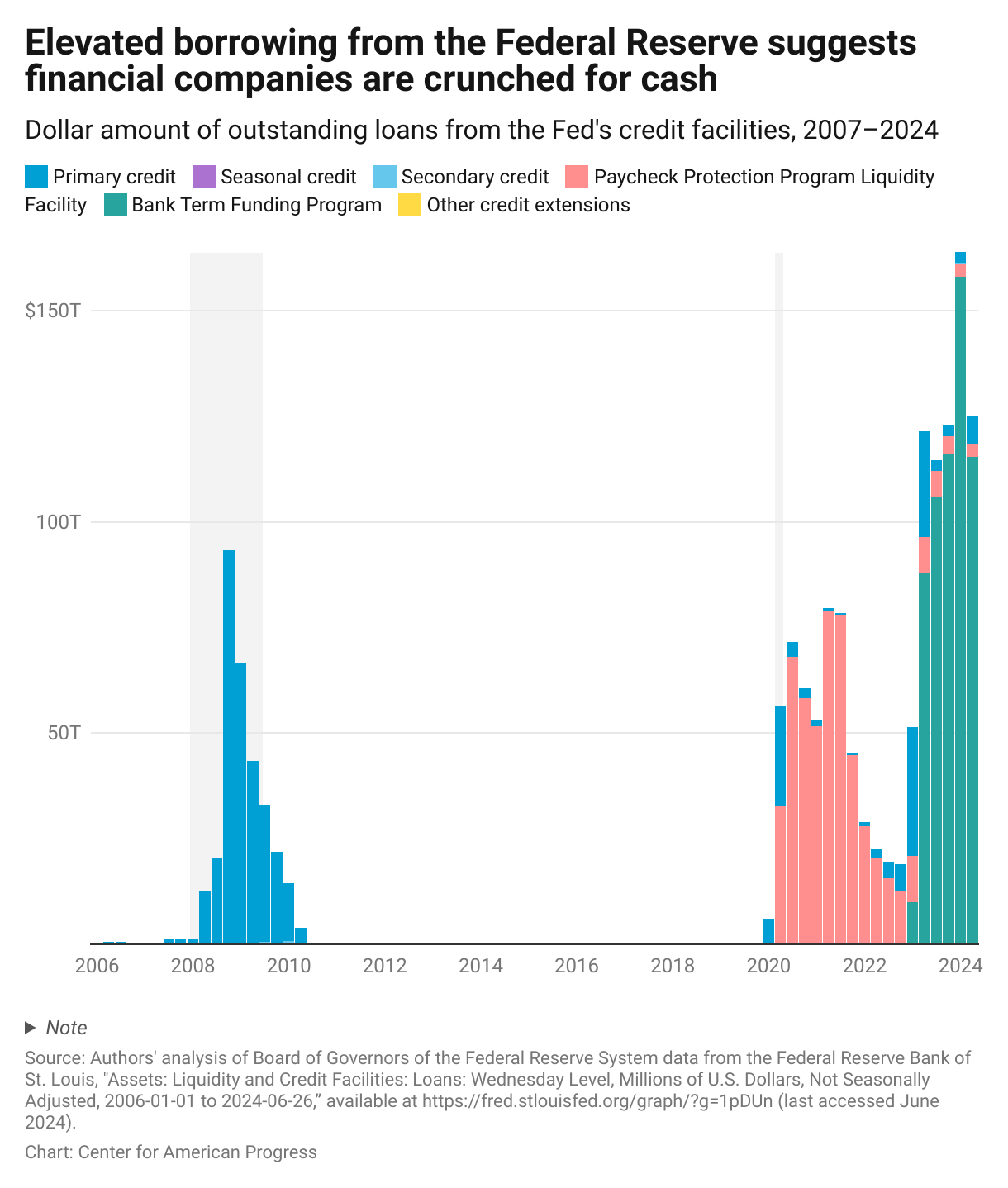

Now, extremists at the far-right Heritage Foundation are laying the foundation for another crisis as part of the organization’s Project 2025. The Project 2025 policy agenda includes a harmful set of proposals intended to increase Wall Street profits. There is an extensive, well-documented set of plans to overturn post-crisis policies that protect consumers, investors, and the stable functioning of financial markets. But the agenda also includes new limits on regulators’ capacity to step in during periods of instability. Specifically, it would restrict the Federal Reserve’s “lender-of-last-resort” function that allows troubled banks to borrow money quickly. This lending backstop has been central to confining the severity of economic harms throughout the financial crisis, during the COVID-19 pandemic, and amid the failures of several midsize banks in early 2023. (For more information, see Figure 1, which displays outstanding lending from the Federal Reserve.)

These policy changes would foster financial market risk-taking while kneecapping regulators’ ability to quell instability. It is easy to see just how irresponsible this is by calculating the present-day costs of a repeat of the Great Recession.

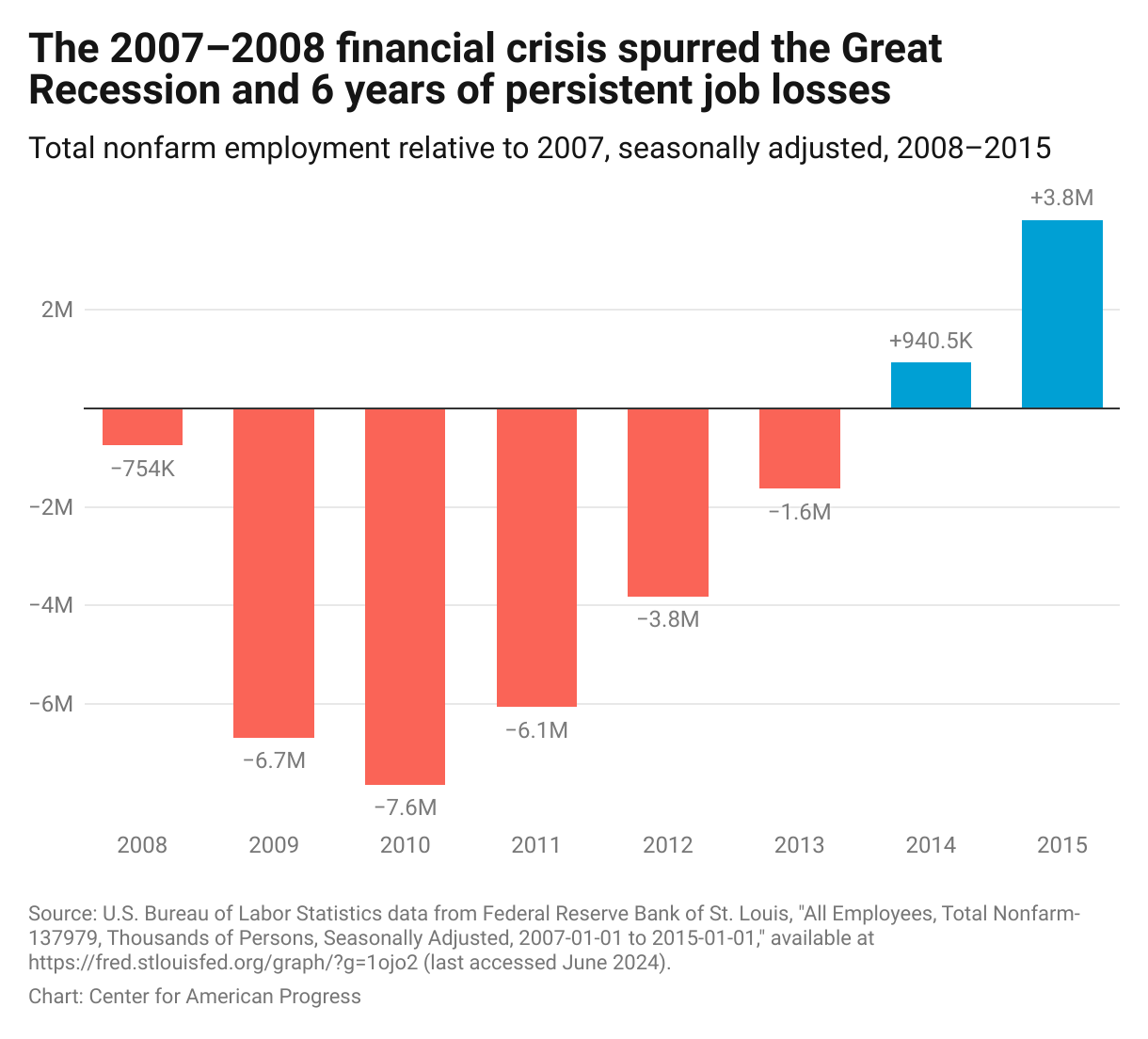

The recession caused by the 2007–2008 financial crisis came at extraordinary costs. Between 2008 and 2009, the United States lost 7.6 million jobs—or 5.5 percent of nonfarm employment—relative to 2007 levels. It took until 2014, more than five years, for employment to recover to pre-crisis levels. (see Figure 2)

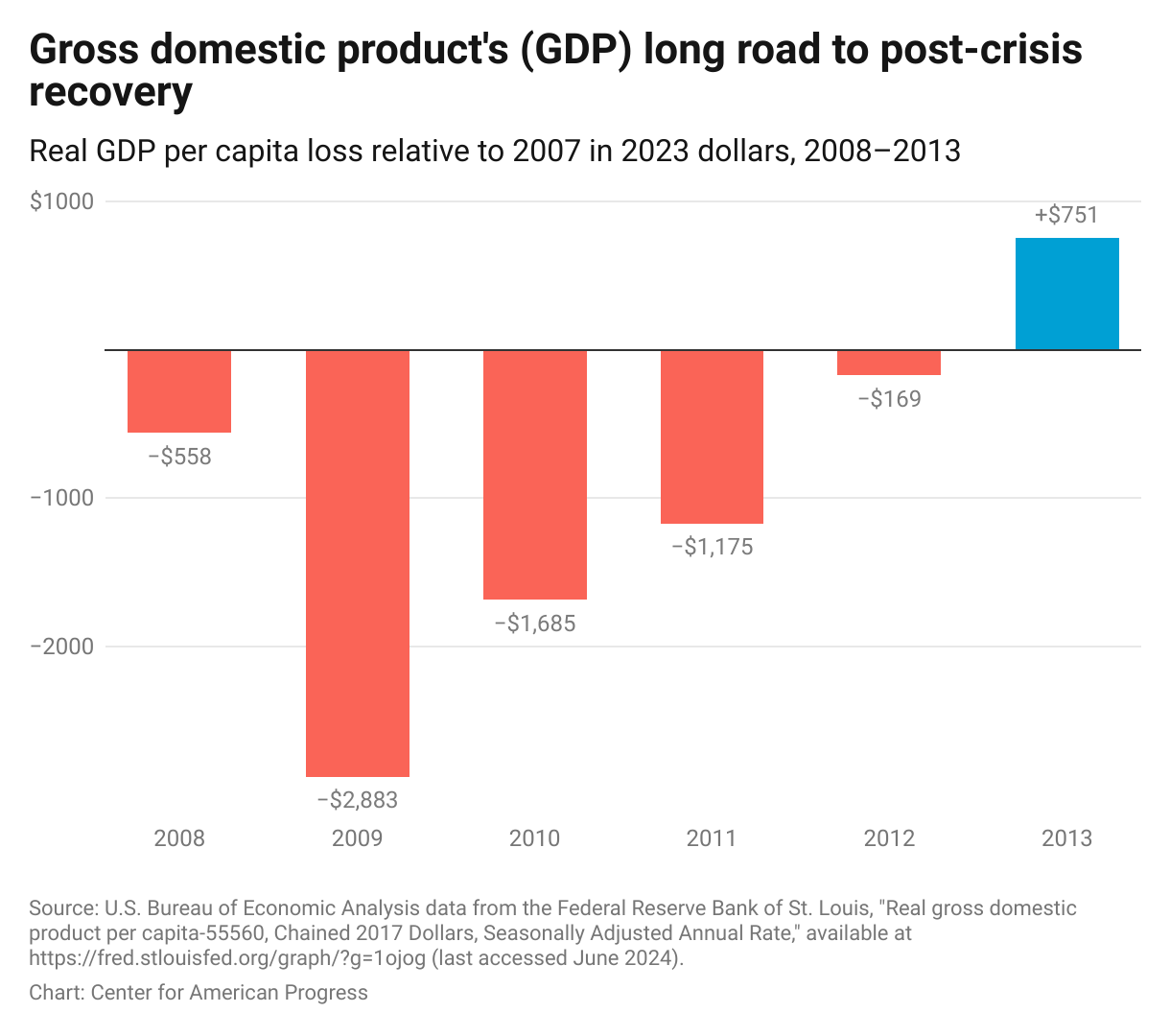

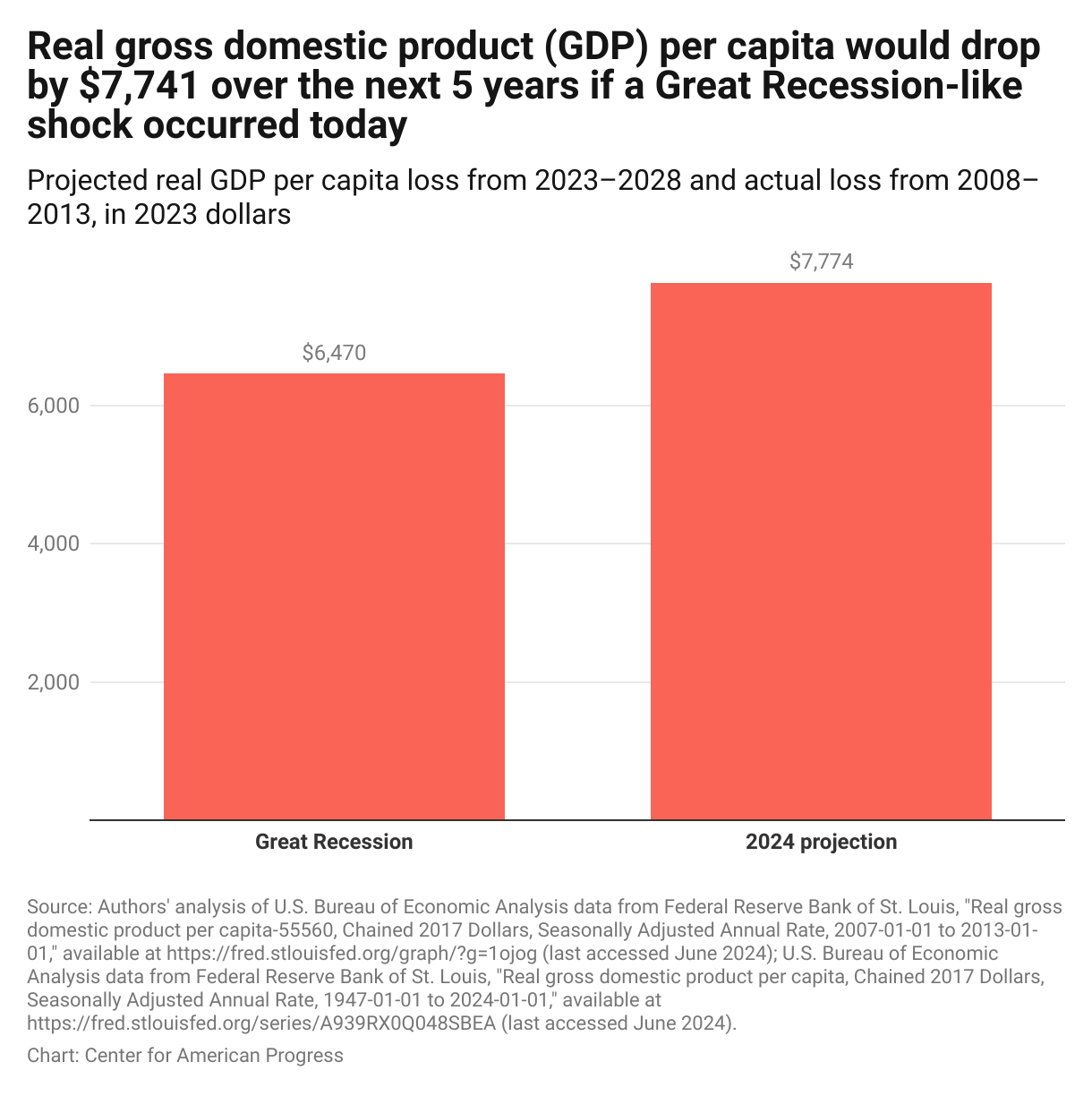

The crisis also caused significant, persistent declines in real gross domestic product (GDP) per capita. (see Figure 3) From 2008 to 2013, GDP per capita remained below the 2007 level. During this period, real per capita losses were $6,470 (in 2023 dollars), equivalent to 9.5 percent of 2007 per capita GDP.*

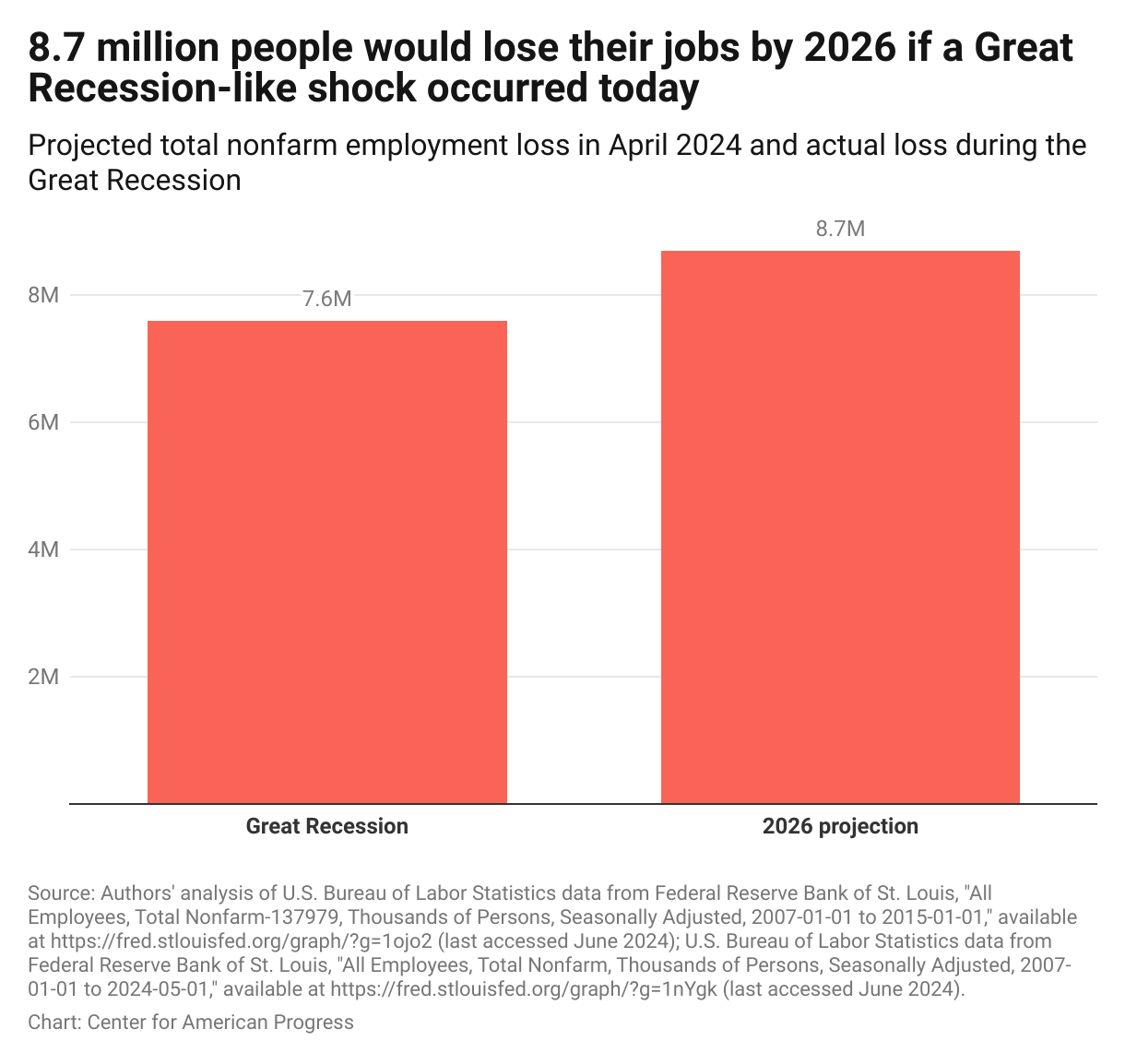

Rolling back rules that require banks and other financial actors to disclose and carefully manage their risks while at the same time hamstringing regulators—especially amid indications that the financial system is currently fragile (see Figure 1)—will make financial crises more likely. CAP finds that 2007-scale financial shock today would result in 8.7 million people losing their jobs by 2026, and employment would not recover to current levels until 2031.** Additionally, the loss in real GDP per capita over the next five years would be $7,774.*** (see Figure 5)

Given the continuing fragility of the financial system, the Project 2025 proposals on financial regulation are dangerous and impossible to justify. They advocate weakened oversight of financial markets, which will make financial shocks more likely. At the same time, they want to limit the Federal Reserve’s ability to contain those shocks. This is a toxic combination. While it may increase short-term profits for some financial market actors, it makes large losses in income and employment more likely.

* There is also evidence that losses in GDP per capita are larger and more persistent than these short-term comparisons suggest. Economists at the Federal Reserve Bank of San Francisco have estimated that the long-term effects of the 2007–2008 crisis led to a lifetime income in present discounted value terms of about $70,000 per capita (in 2017 dollars). These losses are potentially explained by factors such as reduced entry of high-growth potential start-up firms during the crisis, leading to a persistent loss in output. See Regis Barnichon, Christian Matthes, and Alexander Ziegenbein, “The Financial Crisis at 10: Will We Ever Recover?” (San Francisco: Federal Reserve Bank of San Francisco, 2018), available at https://www.frbsf.org/research-and-insights/publications/economic-letter/2018/08/financial-crisis-at-10-years-will-we-ever-recover/; Regis Barnichon, Christian Matthes, and Alexander Ziegenbein, “Are the Effects of Financial Market Disruptions Big or Small?”, Review of Economics and Statistics 104 (3) (2022): 557–570, available at https://cm1518.github.io/files/CS.pdf.

** Estimated as a 5.5 percent decline in total nonfarm employment from the April level of 158,280,000 people.

*** Estimated as 9.5 percent of the 2023 GDP per capita, $81,974.